Merger Control in the UK—Three and a Half Things You Need to Know

Merger control in the UK is changing. With Brexit at the doorstep, COVID-19 still looming, and growing trade tensions across the globe, UK merger reviews will become more prominent, and we believe the UK Competition and Markets Authority (CMA) is becoming more interventionist, despite (or maybe because of) the voluntary nature of the regime.

Core industries continue to be healthcare and the digital sector.1 The CMA is also particularly sensitive where the acquisition involves innovation overlaps between actual or potential competitors.

Below you will find a status update of key changes that might impact your business. The three key changes are that (i) Brexit leads to UK merger filings in cases where previously a filing with the EU would have sufficed, (ii) a new and growing UK foreign direct investment regime will lead to increased scrutiny, and (iii) the CMA is becoming more interventionist in cases. The 'half' change is that the UK leaving the EU can lead to jurisdictional changes outside of the UK in cases that straddle the threshold requirements.

Brexit—the End of the EUMR "One-Stop-Shop" Principle for the UK

As we previously discussed,2 "Brexit day" on 31 January 2020 did not affect merger control jurisdiction until 31 December 2020, meaning that—pursuant to the "one-stop-shop" principle—until the end of 2020 mergers that satisfy both the EU and the UK jurisdictional test will continue to be reviewed exclusively by the European Commission, including the UK aspects of the deal.

While the exact details of the position in 2021 will depend on the final exit agreement between the EU and the UK, one thing is now a near certainty: as of 1 January 2021, the "one-stop-shop" principle ceases to apply to the UK. This means that any transaction involving UK activities faces the potential for parallel EU and UK investigations. The main implications are twofold: (i) the CMA will conduct its own review of the impact of any mergers in the UK and the Commission's review will no longer cover the UK market(s)—the CMA expects a 40-50% increase in its annual merger workload as a result; and (ii) UK turnover will no longer count towards the EU jurisdictional thresholds.

Here is what you need to know in the run-up to the end of 2020:

- Which date determines jurisdictions? The date of formal notification is key: the Commission will maintain exclusive jurisdiction over deals which are formally registered (i.e., "on the clock") by the end of 2020.3 Given the Commission's last working day of the year is 23 December, only for deals which are notified, and jurisdiction by the Commission accepted, no later than 23 December 2020 will the "one-stop-shop" principle continue to apply. Transactions which were notified to an EU member state and subsequently referred to and accepted by the Commission before 23 December will also remain within the exclusive purview of the Commission.

In practice, this means that any deal from now on will need to factor in the jurisdictional change, as (potentially lengthy) pre-notification discussions with the Commission are required to avoid the filing being rejected as incomplete.

- How will the thresholds change? After the "one-stop-shop" principle ceases to apply on 31 December 2020, turnover generated in the UK will no longer be included for the purpose of the EU thresholds. This means that some transactions which meet the EU test only when UK turnover is counted may end up needing to be filed with a number of EU national competition authorities instead.

In such a case, the parties need to consider their filing strategy of whether to file before or after 1 January 2021, and whether to seek a referral of the case between the EU and EU member states.

- Will the UK merger control regime change after Brexit? As also previously discussed,4 the UK regime is and will remain voluntary—meaning that, even where the jurisdictional thresholds are met, no filing is required and deals can be closed prior to CMA clearance. Nevertheless, to ensure that, post-Brexit, the CMA can work effectively with other competition authorities on large multi-jurisdictional mergers, the CMA has started exploring whether transactions above a certain threshold should be subject to mandatory notification, paired with a "standstill" obligation.5

If this proposal were to be implemented, parties would no longer be able to take antitrust risk in the UK and close whilst merger clearance is pending, or in the absence of it.

In any event, the CMA now regularly makes use of its powers to obtain hold-separate undertakings pending a merger review and we expect this trend to continue.

- Implications for transactions that straddle the period December 2020–January 2021. In anticipation of potentially conducting its own review after December 2020, the CMA is encouraging merging parties to engage with it "significantly in advance of the end of the transition period", particularly where a merger may raise potential UK competition concerns. The CMA is also monitoring cases that are in pre-notification with the Commission, and it has become rather common for it to ask for information about the transaction and/or a copy of merger filings in parallel to the EU review.

For deals which risk not being on the clock by December 23 and which are likely to meet the UK jurisdictional threshold, parties should therefore start planning constructive engagement with the CMA (including by sharing draft EC notifications) to avoid the risk of significant delays if formal notification were indeed to stray into 2021. The CMA has so far shown to be pragmatic and open to dialogue.

The potential change in jurisdiction will need to be considered in the transaction documents, especially in relation to conditions precedent and long stop dates.

Expanded UK Government Intervention in Foreign Transactions

As we previously discussed,6 in line with the general trend at the global level, in the last couple of years the UK government has been increasing its power to intervene in relation to foreign acquisitions over and above competition-based considerations.

There are currently no specific controls on foreign investment in the UK and the UK government can intervene on "public interest" grounds only if a transaction qualifies as a "relevant merger control situation" (i.e., two or more businesses cease to be distinct and the transaction meets the UK turnover and/or share of supply test).7 Up until now, "public interest" considerations allowing for government intervention were national security, plurality of the media, and the stability of the UK financial system.8

In 2018, lower thresholds9 triggering potential review by both the CMA (on competition grounds) and the UK government (on public interest grounds) were introduced with respect to transactions affecting goods and services that can be used for military or military and civilian use, computing hardware and quantum technologies. In parallel, the UK government launched a proposal for a standalone foreign investment control regime—entirely separate from the CMA merger control review, independent of reaching a set jurisdictional threshold, and applicable to all sectors of the UK economy—for transactions raising national security concerns.

With increasing concerns over certain foreign (particularly ex-EU) investments, and following the effects of the COVID-19 pandemic, two reforms have most recently further widened the scope for potential UK government intervention.

- Public health emergencies. On 23 June 2020, the UK government added public health emergencies to the definition of "public interest", allowing the UK government to intervene in any transaction which meets the UK merger control thresholds and involves businesses critical to the UK's "capability to combat, and to mitigate the effects of, public health emergencies"—such as, but not limited to, the present COVID-19 pandemic. The focus of the reform is clearly on transactions where the target of a foreign acquisition is directly involved in the response to a health emergency (such as manufacturers of vaccines, personal protective equipment, or essential medical supplies). However, as the UK government has made clear,10 this is a broad and potentially far-reaching power which could apply across a number of different sectors including information technology and food supply chain, given the potential for increased demand for internet services or for disruption to food supply in a lockdown situation.

The existing (higher) merger control thresholds11 must still be met, meaning that very small UK businesses will not likely be affected.

- Artificial intelligence, cryptographic authentication technology, and advanced materials. On 21 July 2020, the UK government further extended its ability to intervene in deals on national security grounds by adding three new categories of target businesses caught by the lower merger control thresholds12 introduced in June 2018:

a) artificial intelligence (including related research, services, and development);

b) cryptographic authentication technology (i.e., electronic methods of authentication using cryptographic means, where these products are reasonably expected to be used in systems critical for national security); and

c) advanced materials (i.e., material and alloys with breakthroughs and/or specific physical properties).

The above will add uncertainty to any transaction in these sectors as, in addition to the usual assessment whether to notify a transaction to the CMA, firms will also need to factor in the risk that a transaction might be called in for review by the UK government on public interest grounds, with a potential impact on timing, as well as feasibility.

That said, if and when implemented, the longer-term proposed reform to the UK FDI regime launched in 2018 is likely to have a much broader impact than any such ad hoc changes, given that a much larger number of transactions—including those that do not qualify as mergers or do not meet the existing thresholds—could be subject to government review if they raise national security concerns.

Increased Interventionism by the CMA

The CMA's greater readiness, over the past two to three years, to assert jurisdiction over transactions with very limited (if any) UK nexus, as well as to challenge mergers that might previously have been approved unconditionally, is undeniable. This trend is likely to continue post-Brexit, thus potentially affecting a number of larger global deals after the end of the transition period.

Examples of the CMA's expansive approach to jurisdiction include:

- Sabre/Farelogix, where the parties were US businesses with a minimal presence in the UK, and the target had no revenues directly attributable to UK customers and no direct contracts for its services with UK customers. However, Farelogix did have a technical agreement with UK airline British Airways the effect of which was—considered together with other arrangements—that British Airways received supply of Fairlogix' services and met the UK's share of supply test (which is not a market share test).

- Roche/Spark, where the CMA asserted jurisdiction despite the target not having UK sales or customers (and thus existing products that competed with Roche), simply on the basis that Spark was engaged in R&D activities for treatments expected to compete with Roche in the future. The CMA's decision in this case is remarkable in several ways, including (i) the dynamic, forward-looking assessment of the parties' overlaps, with products in Phase II (and in some cases Phase I) clinical trial considered at a sufficiently advanced stage of development to be considered as competing products, and (ii) the way the 25% share of supply test was calculated, using number of UK-based full-time employees engaged in clinical trial activities rather than sales/revenues.

We get a sense that over the last two years the number of outright prohibitions or cases that were abandoned because of a likely prohibition has risen.

In Ecolab/Holchem, the CMA blocked a completed merger in which the combined market share was below 40%, on grounds that the parties were close competitors and the combined entity would be twice as large as its nearest competitor. In this context, the CMA rejected the parties' proposed remedy to transfer some customers and assets to a third-party competitor.

The CMA also very recently prohibited the JD Sports Fashion/Footasylum13 acquisition (a merger of high street sports shops) and ordered the disposal of the Footasylum business in its entirety. In Bottomline/Experian (a merger of payment software and solutions providers), the CMA also required an unwinding in the context of its investigation over the completed acquisition by Bottomline Technologies of Experian's payments gateway business.14

In viagogo/StubHub, the CMA is also currently investigating the completed acquisition by viagogo of the StubHub business of eBay—both globally-active providers of online exchange platforms for buying and selling tickets to live events.15

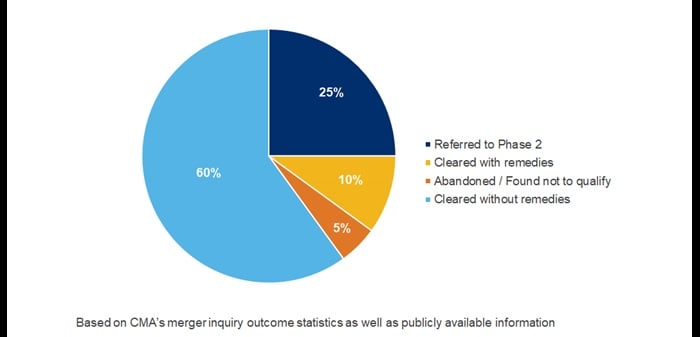

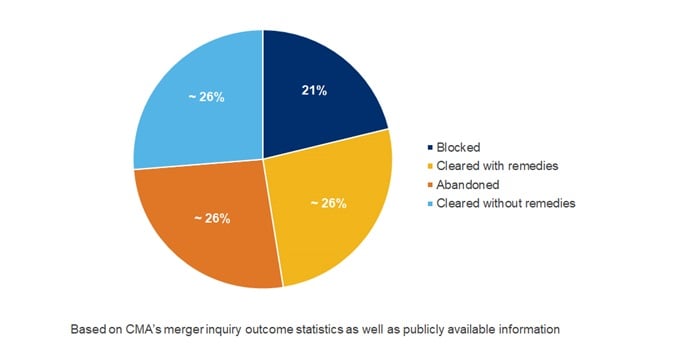

Please see below for a snapshot of recent Phase 1 and Phase 2 UK merger control outcomes.

CMA Phase 1 cases—outcomes from 1 January 2019 to date

CMA Phase 2 cases—outcomes from 1 January 2019 to date

For more details about the UK merger control regime see our previous publications: "UK Merger Control Snapshot and Brexit" and "Merger Control: Expect a More Active UK Authority."

-

This trend is clear from the analysis of recent CMA cases at paragraph 3 of this Advisory. Tackling concerns in digital markets is also one of the CMA's strategic objectives for 2020/2021—see "CMA Annual Plan 2020 to 2021."

-

See Arnold & Porter Advisory, "Brexit and Merger Control: Expect a More Active UK Authority," published on 30 January 2020.

-

The CMA will not have power to "take back" the UK aspects of these deals unless they are referred to it by the Commission under the normal referral mechanisms.

-

See Arnold & Porter Advisory, "UK Merger Control Snapshot," published on 25 September 2019.

-

See letter from the Chair of the CMA to the Secretary of State for Business, Energy and Industrial Strategy (BEIS), published on 25 February 2019.

-

See Arnold & Porter Advisory "Foreign Direct Investment Control in Europe: Helicopter View of an Expanding Landscape," published on 26 February 2019. With specific regard to the UK, see Arnold & Porter Advisory "UK Merger Control: A New Regime for State Intervention, Foreign Acquisitions and National Security," published on 26 July 2018.

-

I.e., a target UK turnover exceeding £70 million and/or the creation of, or an increase to, 25% or more in the parties' combined share of supply.

-

For completeness, the UK government has the power to intervene in a limited number of mergers on the basis of "special" public interest considerations (such as in relation to mergers involving government defence contractors authorised to hold or receive confidential information) even where the standard jurisdictional thresholds relating to turnover and share of supply are not satisfied.

-

I.e., a target UK turnover exceeding £1 million and/or the target meeting (also alone) the 25% share of supply test, with no overlaps with the acquirer and no increment in market share needed.

-

See the explanatory memorandum accompanying the implementing legislation.

-

I.e., a target UK turnover exceeding £70 million and/or the creation of, or an increase to, 25% or more in the parties’ combined share of supply

-

I.e., a target UK turnover exceeding £1 million and/or the target meeting (also alone) the 25% share of supply test, with no overlaps with the acquirer and no increment in market share needed.

-

The investigation concluded on 13 July 2020, with acceptance of JD Sport's undertaking to sell Footasylum.

-

Despite ultimately finding that the transaction would not give rise to competition concerns, the CMA—in the course of its investigation—imposed on the parties an unwinding order requiring Bottomline to segregate all of Experian's commercially sensitive information, thus effectively forcing it to recreate two separate business units with separate management and IT systems.

-

The case is currently undergoing an in-depth investigation, following the CMA's rejection of viagogo's undertakings offered on 18 June 2020.

Key Contacts